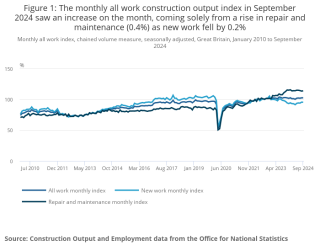

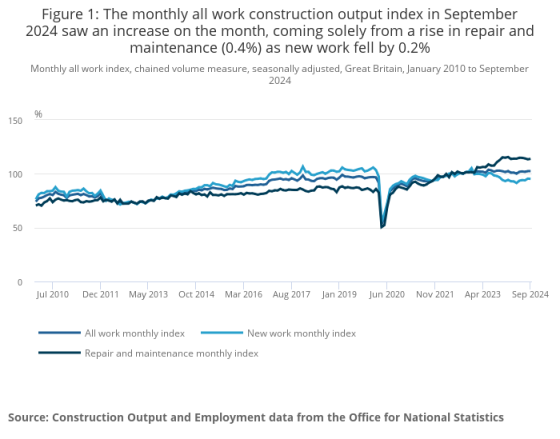

Monthly construction output is estimated to have grown by 0.1% in volume terms in September 2024. This follows growth of 0.6% (revised from 0.4%) in monthly construction output in August 2024 and a fall of 0.4% in July 2024.

September’s growth came from a rise in repair & maintenance (0.4%) as new work fell by 0.2%.

The 0.1% growth in construction output in September 2024 represents an increase of £15m in monetary terms, compared with August 2024, with four out of the nine sectors seeing growth on the month. The volume in September 2024 was £17,654m.

For the three months of July to September 2024, compared with Quarter 2 (April to June), construction output grew 0.8%. This came solely from an increase in new work (2.0%), as repair & maintenance fell by 0.6% over the third quarter.

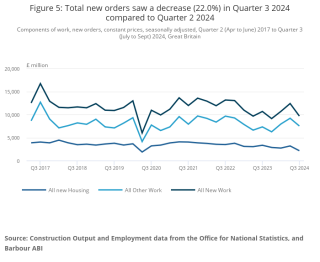

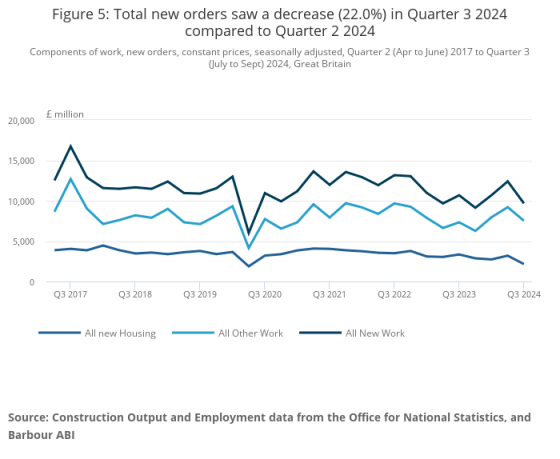

Forward indicators are not looking good, however, with new orders falling 22.0% (£2,722m) in Quarter 3 2024 compared with Quarter 2. This quarterly decrease came mainly from private new housing and private commercial new work, which fell 31.3% (£861m) and 20.8% (£786m), respectively. The other main contributor to the fall in other new work was public new orders, which decreased by 28.0% (£532m).

The 22% fall in orders in Q3 follows a 16% rise in Q2.

Clive Docwra, managing director of property and construction consultancy McBains, said: “Today’s figures are a mix bag for the industry. The good news is that construction outperformed other industry sectors over the third quarter of the year, seeing an 0.8% increase in output compared to GDP overall growing by just 0.1%.

“On the downside, the September figures for construction show a slowdown in growth of just 0.1% compared to August. Furthermore, after housebuilding had seen a recent mini-resurgence, figures show private housing new work in September dropped by 0.4%, while private commercial work fell by 0.1%.

“These decreases could have been as a result of uncertainty ahead of the budget with investors holding off on decisions until the picture becomes clearer. An interest rate cut in December is looking unlikely because of concerns that the borrowing spree outlined in the Budget will fan inflation so costs are likely to remain high, putting some major projects out of commission for the time being.

“However, our clients in many work sectors are still feeling bullish for the long term, and will be hoping this represents merely a blip in the recent recovery.”

Josh Ward-Jones, director of Bloom Building Consultancy, commented: “After a weak first half of the year, construction has surged to become the fastest growing industry in Britain’s slowing economy.

“But construction’s bragging rights come with caveats. The expansion posted in the third quarter came after three successive quarterly falls, so while the turnaround is welcome, total output is still down on where it was at this point in 2023.

“There’s also a two-speed feel to the industry data, with private sector housebuilding stuck in reverse as high interest rates continue to hold back developers’ willingness to buy land and build homes.

“The picture is even more alarming when you look at the pipeline. The value of new orders placed by private sector housebuilders fell by a third on the quarter, and is down by a painful 34.4% compared to Q3 2023.”